Medicare 101 Overview

At Creekstone Benefits, we help you understand your Medicare choices, so you feel empowered to make confident decisions about your health.

What Is Medicare?

Established in 1965, Medicare marked a significant milestone in American healthcare. It was created to provide health insurance for Americans aged 65+, regardless of income or medical history, and lessen the burden of healthcare costs for this segment. Medicare also helps some younger individuals with disabilities or certain health conditions. It’s broken down into various parts that cover different services.

Original Medicare

Original Medicare is a fee-for-service health plan. After you pay a deductible, Medicare pays its share of the Medicare-approved amount, and you pay your percentage (coinsurance). Original Medicare has two parts:

Part A (Hospital Insurance)

Helps cover inpatient hospital stays, skilled nursing facility care, hospice care, and some home health services.

Part B (Medical Insurance)

Helps cover doctor visits, outpatient care, preventive services, and medical supplies.

More Medicare Plans & Programs

Medicare Supplement (Medigap): Works Together with Original Medicare

Medigap plans bridge the coverage gaps left by Medicare Parts A and B to help cover out-of-pocket costs like deductibles, copayments, and coinsurance. A Part D drug plan must be purchased separately.

Part C (Medicare Advantage): An Alternative to Original Medicare

Medicare Part C (Medicare Advantage) combines the benefits of Original Medicare (Parts A and B), often with additional coverage, which varies by plan. Most plans use provider networks (similar to an HMO or PPO).

Part D (Prescription Drug Plans)

Medicare Part D Prescription Drug Plans (PDP) work in tandem with Original Medicare (Part A and Part B) or Medicare Advantage plans to provide prescription drug coverage.

Medicare Enrollment Periods

There are several enrollment periods for Medicare, depending on your situation. Reach out to us for guidance — we can help you understand the right timing for your situation.

Initial Enrollment Period (IEP)

Your first chance to enroll in Medicare when you turn 65:

- Generally the best time to enroll in Parts A and B, or C, and possibly D.

- A seven-month window that starts 3 months before your 65th birthday month, includes your birthday month, and ends 3 months after.

Annual Enrollment Period (AEP)

October 15 – December 7 each year

During the AEP window, you can:

- Join, change, or drop a Medicare Advantage plan;

- Join, change, or drop a Part D drug plan;

- Move from Original Medicare to Medicare Advantage;

- Move from Medicare Advantage to Original Medicare and consider adding a Medigap plan*

Medicare Advantage Open Enrollment (OEP)

January 1 – March 31 each year

If you’re already in a Medicare Advantage plan, you can:

- Switch to another Advantage plan;

- Drop your Medicare Advantage plan and return to Original Medicare (and join a Part D plan and/or a Medigap plan*).

If you’re in Original Medicare, you can’t join a Medicare Advantage plan during this window.

*Important Note: Joining a Medicare Supplement (Medigap) plan after the initial enrollment window may require medical underwriting. This means existing health conditions could cause denied coverage or increased premiums. There are some exceptions, such as losing employer coverage or completing a Medicare Advantage trial period, during which you may have guaranteed issue rights.

Special Enrollment Period (SEP)

You may qualify for an SEP if:

- You move out of your Medicare Advantage or Part D plan’s service area

- You lose group health coverage (such as employer or union)

- You’re newly eligible for Medicaid

Ask us for more information about SEPs.

Medicare Costs

Part A (Hospital Insurance)

You usually don't pay a monthly premium for Medicare Part A (Hospital Insurance) coverage if you or your spouse paid Medicare taxes while working. This is sometimes called "premium-free Part A." Most people get premium-free Part A. Click here for more detailed information on Part A costs.

Part B (Physician Insurance)

You pay a premium each month for Part B. If you get Social Security, Railroad Retirement Board, or Office of Personnel Management benefits, your Part B premium will be automatically deducted from your benefit payment. If you don’t get these benefit payments, you’ll get a bill.

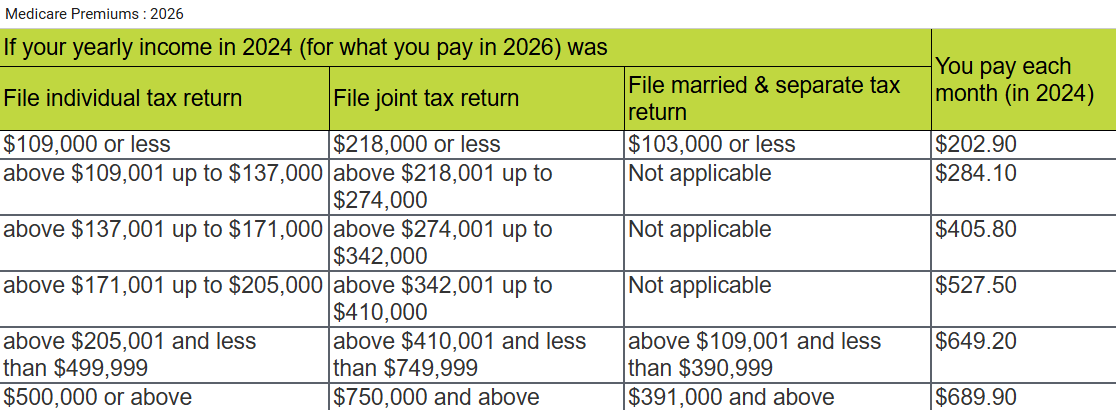

Most people will pay the standard premium amount. If your modified adjusted gross income is above a certain amount, you may pay an Income Related Monthly Adjustment Amount (IRMAA). Medicare uses the modified adjusted gross income reported on your IRS tax return from 2 years ago (the most recent tax return information provided to Social Security by the IRS).

If you're in 1 of these 5 groups, here's what you'll pay:

In 2026 you pay $202.90 for your Part B deductible. After you meet your deductible for the year, you typically pay 20% of the Medicare-Approved Amount for these:

- Most doctor services (including most doctor services while you're a hospital inpatient)

- Outpatient therapy

- Ambulance Services

- Limited outpatient Prescription Drugs

- Durable Medical Equipment (DME)

If you're in a Medicare Advantage Plan or other Medicare plan, your plan may have different rules. But your plan must give you at least the same coverage as Original Medicare.

Glossary of Common Medicare Terms

Here we’ll explain some common Medicare terms you may come across as you look at plans and policies.

Advance Beneficiary Notice (ABN)

A notice from your provider if they think Original Medicare may not pay for a service. Allows you to decide whether to proceed and pay out of pocket.Assignment

When a provider agrees to accept Medicare’s approved amount as full payment.Copayment (Copay)

A fixed dollar amount you pay for a covered service (like $20 for a doctor visit).Coinsurance

Your share of the costs for a covered service, usually a percentage (like 20%).Coverage Determination (Part D)

A decision your drug plan makes about whether it will cover a drug and what you’ll pay for it.Creditable Coverage

Drug coverage (an employer plan, VA benefits, or other) that’s determined to be at least as good as Medicare Part D coverage. Helps you avoid enrollment penalties. See the Medicare > Prescription Drug Plans page for more information.Durable Medical Equipment (DME)

Medical items ordered by a physician for you to use at home, such as wheelchairs, walkers, oxygen machines, etc.Deductible

The amount you pay out of pocket during a calendar year before your plan starts to pay benefits.

Emergency Care

Care needed immediately for a life-threatening injury or illness (such as chest pain, trouble breathing, severe bleeding, or signs of a stroke). Covered anywhere in the U.S., even outside your plan’s network (if you are in a Medicare Advantage plan).Guaranteed Issue Rights

Your right to enroll in a Medigap policy without being denied or charged a higher premium based on existing health conditions. You get this right during standard enrollment periods and special situations.Lifetime Reserve Days

Extra hospital days Medicare covers after you use up your regular hospital coverage. You will pay a daily copayment. This is limited to 60 days over your lifetime.Limiting Charge

A cap on what some doctors can charge you in the case that they don’t accept Medicare assignment.Medicare Summary Notice (MSN)

A statement you get every three months if you are in Original Medicare showing what Medicare paid for services and what you may owe.Premium

The monthly amount you pay for your Original Medicare or Medicare plan. You may have separate premiums for a Medigap plan, a Medicare Advantage plan, or a Part D drug plan.Prior Authorization

Approval required by some plans in order for the plan to cover a certain service or medication. This approval must be obtained from the insurance company.Urgently Needed Care

Care you need soon for a sudden illness or injury that isn’t life-threatening (such as a sprained wrist, minor cut, or respiratory infection while traveling). Usually covered even if you’re out of your Medicare Advantage plan’s service area.